Buying a home is a major financial milestone, but having bad credit can make the process more challenging. A less-than-perfect credit score can limit your options, resulting in higher interest rates or even difficulty getting approved for a mortgage. However, bad credit doesn’t have to stop you from achieving your dream of homeownership. With the right strategies and a proactive approach, you can improve your chances of securing a mortgage and finding a home that fits your needs and budget.

Bad credit is often defined as a credit score below 620, although the specific cutoff can vary depending on the lender and the type of loan. A low credit score typically indicates a history of missed payments, high levels of debt, or other financial issues. Lenders view borrowers with bad credit as higher risk, which is why they may offer less favorable terms. Despite these challenges, there are steps you can take to improve your situation and increase your likelihood of mortgage approval.

Improving Your Credit Score Before Applying

One of the most effective ways to improve your chances of securing a mortgage with bad credit is to work on boosting your credit score before you apply. Even a small increase in your score can make a significant difference in the mortgage terms you’re offered. Start by obtaining a copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—and review them for errors. If you find any inaccuracies, dispute them to have them corrected.

Next, focus on paying down existing debt, especially credit card balances. Reducing your credit utilization ratio—the amount of credit you’re using compared to your total credit limit—can help raise your credit score. Additionally, make sure all your bills are paid on time going forward, as consistent on-time payments are crucial for improving your credit.

If possible, avoid opening new credit accounts in the months leading up to your mortgage application, as this can result in hard inquiries on your credit report and temporarily lower your score. By taking these steps, you can improve your credit profile and increase your chances of qualifying for a mortgage with better terms.

Exploring Different Mortgage Options

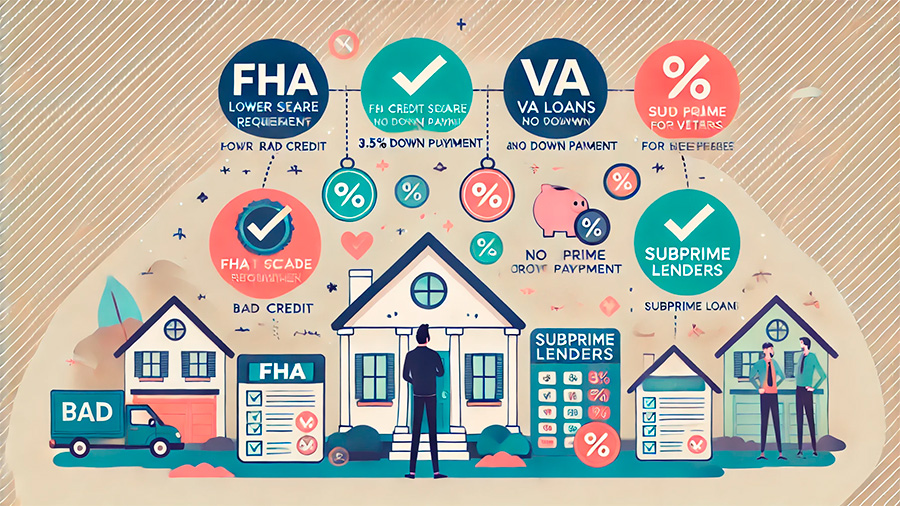

When you have bad credit, it’s important to explore all available mortgage options, as some may be more accessible than others. Certain loan programs are specifically designed to help individuals with less-than-perfect credit achieve homeownership.

One option to consider is an FHA loan, which is insured by the Federal Housing Administration. FHA loans are more lenient in their credit score requirements, often allowing scores as low as 580 with a 3.5% down payment, or even lower with a larger down payment. Because the FHA guarantees these loans, lenders are more willing to offer them to borrowers with bad credit.

Another option is a VA loan, available to veterans, active-duty service members, and eligible spouses. VA loans are backed by the Department of Veterans Affairs and typically do not require a down payment or mortgage insurance, and they have more flexible credit requirements.

For those who may not qualify for FHA or VA loans, there are also subprime lenders who specialize in offering mortgages to individuals with bad credit. However, it’s important to be cautious when working with subprime lenders, as they often charge higher interest rates and fees. Be sure to compare offers from multiple lenders to ensure you’re getting the best deal possible.

Considering a Larger Down Payment

If your credit score is holding you back, one way to improve your mortgage application is by making a larger down payment. A larger down payment reduces the lender’s risk, which can make them more willing to approve your loan, even with a lower credit score. Additionally, a larger down payment can help you qualify for better interest rates and reduce the amount you need to borrow.

For many buyers with bad credit, saving for a larger down payment may require some time and effort, but it can be worth it in the long run. Consider setting a budget and prioritizing savings to build up your down payment fund. You might also explore down payment assistance programs, which are available in many areas to help first-time homebuyers or those with lower incomes.

Getting Pre-Approved and Shopping Around

Before you start house hunting, it’s a good idea to get pre-approved for a mortgage. Pre-approval gives you a clear understanding of how much you can afford to borrow and shows sellers that you’re a serious buyer. It also provides an opportunity to shop around and compare offers from different lenders.

When you have bad credit, shopping around for a mortgage is especially important. Interest rates and terms can vary significantly between lenders, so it’s crucial to compare multiple offers to find the best deal. Be sure to look at the annual percentage rate (APR), which includes both the interest rate and any fees, to get a true sense of the cost of the loan.

During the pre-approval process, be prepared to provide documentation of your income, assets, and debts. Lenders will use this information, along with your credit score, to determine how much they are willing to lend you and at what interest rate.

Working with a Mortgage Broker or Specialist

If you’re struggling to find a mortgage on your own, consider working with a mortgage broker or specialist who has experience helping borrowers with bad credit. A mortgage broker acts as an intermediary between you and potential lenders, helping you find the best mortgage options based on your financial situation. They can offer access to a wider range of loan products and may have relationships with lenders who are more willing to work with borrowers with less-than-perfect credit.

While there may be fees associated with using a mortgage broker, the expertise and access they provide can be invaluable, especially if you’re having difficulty securing a mortgage on your own. Be sure to choose a reputable broker with a track record of success in helping clients with similar credit challenges.

Conclusion

Buying a home with bad credit presents challenges, but it’s not impossible. By improving your credit score, exploring different mortgage options, considering a larger down payment, and shopping around for the best terms, you can increase your chances of securing a mortgage and achieving homeownership. Additionally, working with a mortgage broker or specialist can provide valuable assistance in navigating the process. With careful planning and persistence, you can overcome the obstacles of bad credit and find a home that meets your needs and budget.